ABC analysis is one of the options for analyzing the internal environment of the company. With the help of ABC analysis, you can divide a large amount of data into three groups based on their significance. This will help you clearly see which positions are key for you, as well as identify the strengths and weaknesses of your company. Thanks to its universality, you can apply the ABC analysis method to almost any field of activity.

As a rule, ABC analysis consists of the following steps

Select a Goal

The purpose of the analysis is what your research is aimed at. At this stage, you choose what you should come to as a result of the analysis. You set goals by each company according to their needs, for example: profit growth, inventory optimization, cost reduction, increasing customer loyalty, etc.

Select the Object of ABC Analysis

At this stage, we determine what exactly we will analyze, that is, we choose the type of ABC analysis, and depending on the selected type of ABC analysis, we make a list of objects, for example:

- ABC analysis of sales – list of customers

- Of assortment – product assortment list

- Inventory – inventory list

- ABC analysis of purchased goods – list of purchased goods

- Analysis of supplier – list of suppliers, etc.

Usually, such lists you can generate from internal automated systems of companies.

Definition of the Parameter

Here we define the indicator by which the object will be analyzed. Depending on the type of ABC analysis, this can be: the amount of sales, margin profit, turnover of the product group, the average inventory, the cost of purchased raw materials, the average settlement period, the average debt, etc.

Ranking

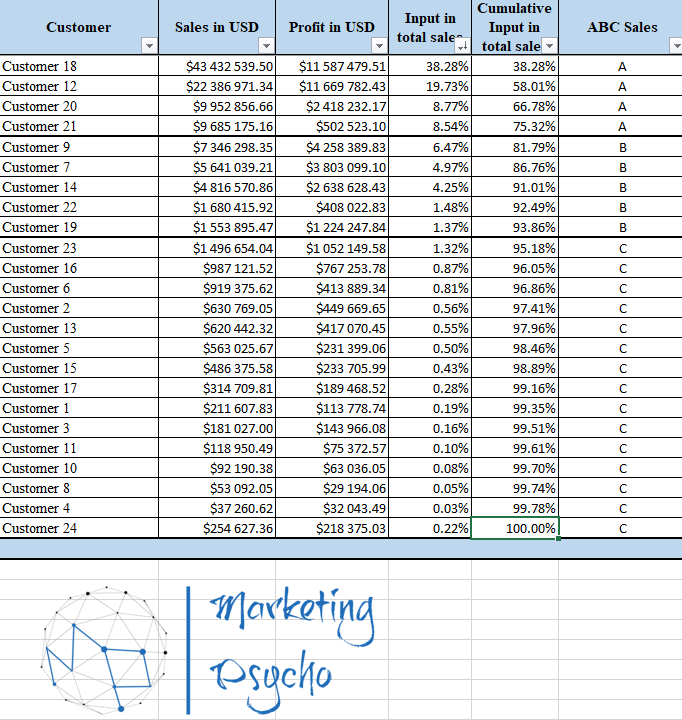

Now we need to sort our list according to the selected parameter in descending order. For example, for ABC analysis of sales with the sales amount parameter, we sort the list from the customers with the highest volume of purchases to the lowest. Then we calculate the total amount for the selected parameter, in our case, the sales amount, and calculate the share of each list item in the total amount. After that, we calculate the share of the sales amount from the total sales amount with a cumulative total. The share with the cumulative total is calculated by adding the parameter to the sum of the previous parameters. For the last item in the list, the cumulative share will be 100%.

Definition of Groups A, B, C

After we have done the ranking of our list, we need to divide it into groups. The definition of groups is based on the Pareto Principle: 20% of the effort provides 80% of the result. In accordance with this, groups in ABC analyses are divided into three types:

A: 80% of sales are provided by 20% of customers. The upper limit of group A is the first position of the list. The lower limit is the percentage of the selected parameter closer to 80% (cumulative total).

B: 15% of sales is provided by 30% of customers. The next position after the lower limit of group A will be the upper limit of group B. And the lower limit of group B will be the position with a cumulative total closer to 95%.

C: 5% of sales provide 50% of customers. The positions of group C, respectively, are all the remaining positions after the lower limit of group B.

You can replace the sales and customers metrics with the ones that are right for you. It is worth noting that the boundaries of the 80% -15% -5% groups can be changed and can be set individually by each company.

Analysis

Once we have divided the list into groups, we can analyze the data and make a decision about each group. The decision will also depend on the purpose of the analysis.

Group A is important. This type of resource should be controlled and monitored, as it is the main source of profit for the company. You should allocate maximum investments for this group. The success of group A is to be analyzed and transferred to other categories.

Group B is necessary. This type of resources is also important for the company, as it brings a stable profit, which allows the company to exist. Investments in this type of company’s resources are not significant and are only necessary to maintain the existing level.

The group C is unimportant. This type of resource usually does not bring much income. Analyzing this group, it is necessary to understand the reason for the low return from this category. If the cause can be eliminated and it is possible to transfer the resource to a higher category, then it is worth trying to do so. If this resource bears only losses, then it is better to get rid of it.

Despite the simplicity of the ABC analysis, it is important to observe certain conditions when compiling it, otherwise the data obtained may not correctly reflect the current state of affairs.

- it is necessary to include similar groups in the analysis

- you must select a specific time interval

- it is necessary to take into account the novelty (customer, product, supplier)

To make it easier for you I’ve prepared the ABC Analysis template which you can download in the Resources section of the website. Now you can run ABC analysis in no time using Apple Numbers template or Microsoft Excel template. You just need to fill in your data instead of what I used.

To find more marketing analysis tips go to Marketing Analysis section of the website.